In 2015, I walked away from the world of procurement SaaS to help a French sustainability software startup crack the US market. By coincidence, it was the same year the United Nations launched the Sustainable Development Goals.

At the time, the SDGs felt like a masterpiece of choice architecture. The UN had taken 17 existential threats and turned them into colourful, manageable tiles — the ultimate “nudge” to align global business with planetary survival. By 2017, I found myself at the UN hosting a panel on how businesses and supply chains can translate these aspirations into day-to-day operations.

Fast forward to January 2026. The nudge became a shove, and the coordination has frayed.

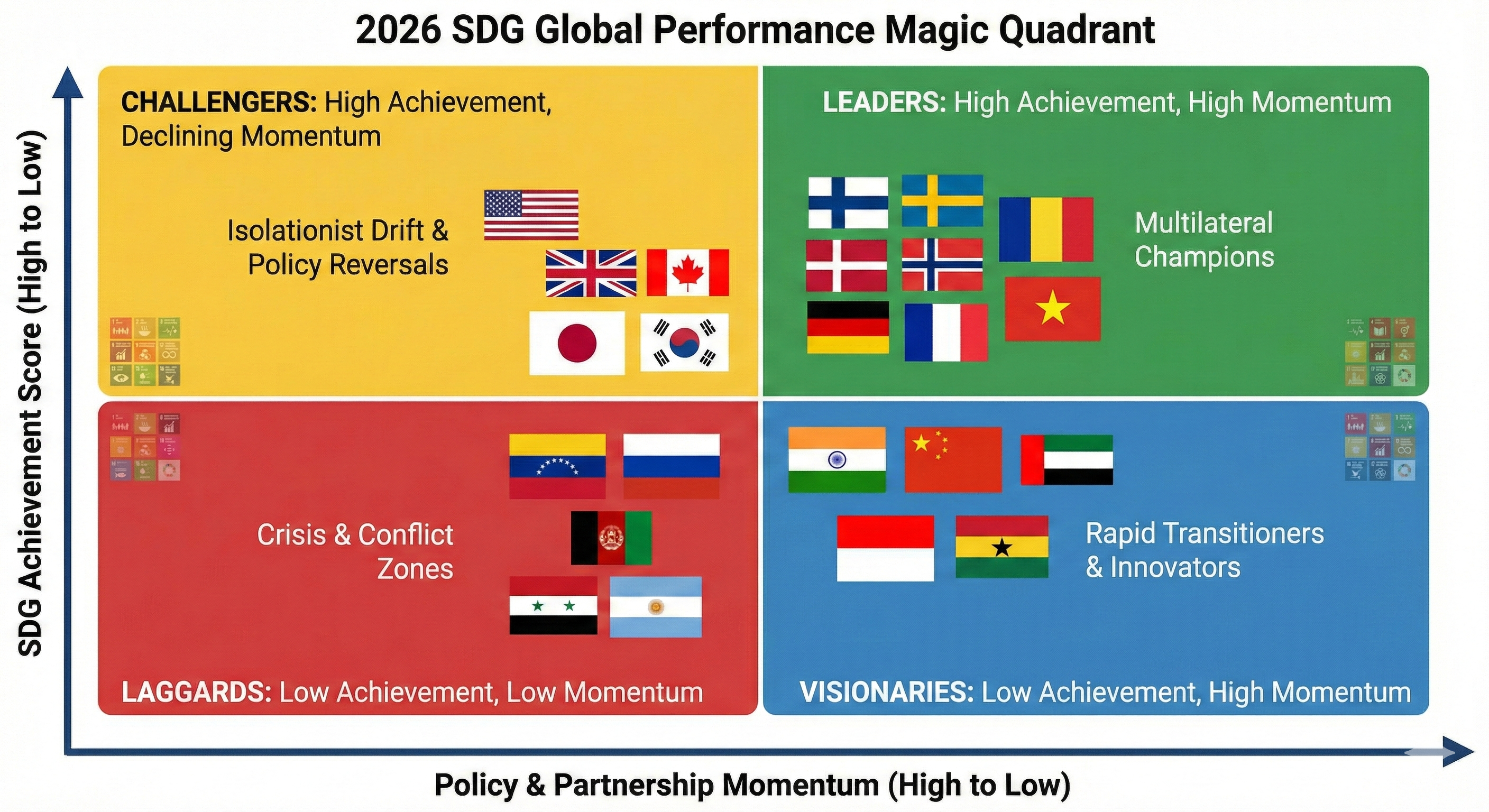

How to Read the 2026 SDG Performance Matrix

The 2026 SDG Global Performance Matrix ranks 50 economies across two dimensions:

Y-Axis — SDG Achievement (the “Hardware”): A country’s cumulative score across all 17 goals. This reflects legacy assets, wealth, and established infrastructure.

X-Axis — Institutional Momentum (the “Software”): A three-year trajectory reflecting commitment to multilateralism, trade positioning, and future-readiness.

The matrix reveals that we are not suffering from a lack of data. We are witnessing a fundamental shift in what drives economic competitiveness.

Leaders: Consistency as a Strategic Asset

A small group of countries demonstrates that institutional continuity is now a source of competitive trade positioning — not just a moral position.

The Nordic bloc — Finland, Sweden, and Denmark — leads by stepping in to fill the $4B+ funding gaps left by withdrawing nations. For businesses, these nations now offer a distinct cost-of-capital advantage; they represent the only remaining stable defaults for global investors fleeing uncertainty elsewhere.

The European core — Germany and France — has doubled down on green industrial policy as a defensive economic strategy. This isn’t altruism. It’s energy independence and supply chain security in a fractured world.

Vietnam is the breakout performer of the decade. Its aggressive renewable deployment has allowed it to leapfrog legacy infrastructure constraints, proving that momentum is not the exclusive domain of wealthy nations.

Challengers: The High Cost of Drift

The top-left quadrant is where nations with high baseline capacity are losing direction fastest.

The United States remains high on achievement due to its sheer economic scale and historical R&D investment. But it sits firmly in the Challenger quadrant — and the trajectory is accelerating downward. By withdrawing from 60+ international bodies, the US has introduced a “standardisation vacuum” that makes its high achievement scores increasingly fragile. The practical result for multinational procurement teams: a growing risk premium on US-based supplier relationships and an erosion of the trade standards the US historically helped set.

The UK and Japan are caught in the cross-currents of trade uncertainty, where alignment with global goals is increasingly viewed through a lens of economic risk rather than strategic opportunity.

Visionaries: Momentum Without Legacy

India and Vietnam are using SDG alignment as a deliberate trade-positioning strategy — building the digital and green infrastructure of tomorrow without the institutional complexity of the West. Capital fleeing the Challenger nations is landing here.

The Gulf States — the UAE and Saudi Arabia — are leveraging sovereign wealth funds to pivot toward green energy at a pace that most nations cannot match. The persistent friction: a Social Deficit around labour rights and civil liberties that prevents their world-class physical infrastructure from reaching full integration with the Leader quadrant.

What This Means for Your Organisation

The SDG framework was never just a UN project. For procurement and supply chain leaders, it was always the most comprehensive map of systemic risk ever published.

In 2026, the businesses that will compound their advantage are those treating SDG alignment as a hard competitiveness signal — not a compliance checkbox. Here’s the practical read:

Supplier geography is geopolitical strategy. The Challenger nations are generating new procurement risk. Supplier diversification toward Leader and Visionary economies is no longer idealism — it’s risk management.

Consistency is the new competitive moat. In a world where the rules are being rewritten, the organisations that have maintained coherent sustainability commitments across the last decade now have a decade’s worth of trusted partnerships, better financing terms, and lower regulatory exposure.

Radical pragmatism over perfect consensus. As former Bank of England Governor Mark Carney put it at Davos: “Nostalgia is not a strategy.” The winning approach is not to wait for a return to the old multilateral order, but to build coalitions and co-invest in resilience now.

The SDGs remain the best brief we’ve ever been given. In 2026, the winners won’t be the ones with the most raw force — they’ll be the ones with the institutional software to survive a fractured world.

Methodology: Achievement scores based on the 2025 Sustainable Development Report and SDG Index (dashboards.sdgindex.org). Financial tracking via the UN Financial Tracking Service and Focus 2030. Geopolitical risk data synthesised from the International Crisis Group and the UN Human Rights Council.